Bond Features and Theories

Bond Features and Prices

Bonds are debt securities – the

bondholder is a creditor of the entity issuing the bond. The bondholder makes a

loan of the face value to the issuer. The issuer (borrower) promises to repay

to the lender (investor) the principal on maturity date plus coupon interest

over its life.

Bond

terms

Par value (face

value): Face amount paid at maturity.

Coupon rate:

Percentage of the par value that will be paid out annually in the form of

interest.

Annual interest

payment on bond = coupon rate par value

Maturity: The

duration of time until the par value must be repaid.

Example

A bond with par

value of $1,000 and coupon rate of 8% might be sold to a buyer for ` 1,000. The bondholder is then entitled to a

payment of ` 80 (= 8% ` 1,000) per year, for the stated life of the bond, say

30 years. The ` 80 payment typically comes in two semi-annual instalments of `

40 each. At the end of the 30-year life of the bond, the issuer also pays the `

1,000 par value to the bondholder.

Call Provisions on

Corporate Bonds

The call provision allows the

issuer to repurchase the bond at a specified call price before the maturity

date. If a company issues a bond with a high coupon rate, when market interest

rates are high, and interest rates later fall, the firm might like to retire

the high-coupon debt and issue new bonds at a lower coupon rate to reduce

interest payments. This is called refunding. The call price of a

bond is commonly set at an initial level near par value plus one annual coupon

payment. The call price falls as time passes, gradually approaching par value.

Callable bonds typically come

with a period of call protection, an initial time during which the bonds are

not callable. Such bonds are referred to as deferred callable bonds. The

option to call the bond is valuable to the firm, allowing it to buy back the

bonds and refinance at lower interest rates when market interest rates fall.

From the bondholder’s perspective, the proceeds then will have to be reinvested

in a lower interest rate. To compensate investors for

this risk, callable bonds are issued with higher coupon rates and promised

yields than non-callable bonds.

Convertible Bonds

Convertible bonds give the

bondholders an option to exchange each bond for a specified number of shares of

common stocks of the firm. The conversion ratio gives the number of

shares for which each bond may be exchanged. Suppose a convertible bond that is

issued at par value of $1,000 is convertible into 40 shares of a firm's stock.

The current stock price is $20 per share, so the option to convert is not

profitable now. However, should the stock price later rise to $30, each bond

may be converted profitably into $1,200 worth of stock.

The market conversion value is

the current value of the shares for which the bonds may be exchanged. At the

$20 stock price, the bond’s conversion value is $800. The conversion premium

is the excess of the bond value over its conversion value. If the bond is

selling currently at $950, its premium will be $150.

Valuation of Bonds

To value a security, we discount

its expected cash flows by the appropriate discount rate. The cash flows from a

bond consist of coupon payments until the maturity date plus the final payment

of par value.

Where r is the interest

rate that is appropriate for discounting cash flows and T is the

maturity date. The present value (PV) of a `

1 annuity that lasts for T periods when the interest rate equals r

is:

Price-Yield Relationship

Nominal yield: This is simply the

yield stated on the bond’s coupon. If the coupon is paying 5%, the bondholder

receives 5%.

Current yield: Current yield = Annual

interest/Current price. This calculation takes into consideration the bond

market price fluctuations and represents the present yield that a bond buyer

would receive upon purchasing a bond at a given price. As mentioned

above, bond market prices move up and down with interest rate changes. If the

bond is selling for a discount, then the current yield will be greater than the

coupon rate. For instance, an 8% bond selling at par has a current yield that

is equivalent to its nominal yield, or 8%.

Current Yield =

Annual interest/Current price = (8% x `

1000) / ` 1000 = 8%.

However, a bond that is selling for less than par, or

at a discount, has a current yield that is higher than the nominal

yield. Thus if you buy a bond with a par value of ` 1000, coupon rate of 8% and

the current price of ` 950, the Current Yield= Annual interest/Current price

= (8 % x ` 1000) / ` 950

= ` 80 / ` 950 = 8.42 %

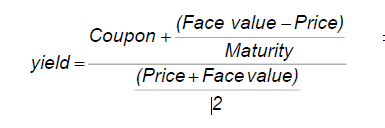

Yield-to-maturity

(YTM): This

measures the investor’s total return if the bond is held to its maturity date.

This includes the annual interest payments plus the difference between what the

investor paid for the bond and the amount of principal received at maturity.

YTM is the annual rate of return

that a bondholder will earn under the assumption that the bond is held to

maturity and the interest payments are reinvested at the YTM. YTM is the same

as the bond’s internal rate of return (IRR). YTM or simply the yield is the

discount rate that equates the current market price of the bond with the sum of

the present value of all cash flows expected from this investment.

Previously, we had calculated the

price of bond value when the discount rate (r) was given. This discount rate

was the YTM. In YTM calculations, the market price of the bond is given, and we

have to calculate the discount rate that equates the present values of all the

coupon payments and the principal repayment to the market price.

We do this by using trial and

error or an approximation formula.

Yield-to-Call: When a bond is

callable, the market also looks to the yield-to-call (YTC). Normally if a bond

is called, the bondholder is paid a premium over the face value (known as the

call premium). YTC calculation assumes that the bond will be called, so the

time for which the cash flows (coupon and principal) occur is shortened. YTC is

calculated exactly like YTM, except that the call premium is added to the face

value for calculating the redemption value, and the first call date is used

instead of the maturity date.

Risks in Debt Securities

Interest rate risk: The cash flows from a

bond (coupon payments and principal repayment) remain fixed though interest

rate keeps changing. As a result, the value of a bond fluctuates. Thus interest

rate risk arises because the changes in the market interest rates affect the

value of the bond. The return on a bond comes from coupons payments, the

interest earned from re-investing coupons (interest on interest), and capital

gains. Since coupon payments are fixed, a change in the interest rates affects

interest on interest and capital gains or losses. An increase in interest rates

decreases the price of a bond (capital loss) but increases the interest

received on reinvested coupon payments (interest on interest). A decrease in

interest rates increases the price of a bond (capital gain) but decreases the

interest received on reinvested coupon payments.

Thus there are

two components of Interest rate risk.

Reinvestment

rate risk is the uncertainty about future or target date portfolio

value that results from the need to reinvest bond coupons at yields that are

not known in advance.

Interest rate

increases tend to decrease bond prices (price risk) but increase the future

value of reinvested coupons (reinvestment rate risk), and vice versa.

Default

risk or credit risk refers to the possibility of having the issuer defaulting on

the payments of the bond. It is the risk that the borrower will not honour, in

full or in part, its promise to repay the interest and principal. The realised

return on a bond will deviate from the expected return if the issuer fails to

meet the obligations to make interest and principal payments.

Most investors

do not directly assess a bond’s default risk, but instead use the credit

ratings provided by credit rating agencies such as CRISIL, ICRA, Moody’s and

S&P to evaluate the degree of risk. Credit ratings are the most common

benchmark used when assessing corporate bond default risk. These securities are

backed by the issuing companies, rather than by government/agency guarantees or

insurance. Credit ratings provide an indication of an issuer's ability to make

timely interest and principal payments on a bond.

The two most

recognised rating agencies, known worldwide, that assign credit ratings to

corporate bond issuers are Moody's Investors Service (Moody’s) and Standard

& Poor's Corporation (S&P). In India, the credit rating agencies are

ICRA and CRISIL among others.

Call

risk: If a company issues a bond with a high coupon rate when

market interest rates are high, and interest rates later fall, the firm might

like to retire the high-coupon debt and issue new bonds at a lower coupon rate

to reduce interest payments. If a bond has a call provision, then the company can

repurchase the bond at a specified call price before the maturity date.

From the bondholder’s perspective it is a disadvantage, as the proceeds will

then have to be reinvested at a lower interest rate. This is the call risk

faced by the bondholder.

Liquidity

risk: Bonds have varying degrees of liquidity. There is an enormous

number of bond issues most of which do not trade on a regular basis. As a

result, if a bondholder wants to sell quickly, he will probably not get a good

price for his bond. This is the liquidity risk.

Duration of Bonds

Bond duration is a measure of bond

price volatility, which captures both price and reinvestment risk and which is

used to indicate how a bond will react in different interest rate environments.

The duration of a bond is the

weighted average maturity of cash flow stream, where the weights are

proportional to the present value of cash flows. It is defined as:

Duration = D = {PV (C1) x 1 + PV

(C2) x 2+ ----- PV (Cn) x n} / Current price of the bond

Where PV (Ci) is the present

values of cash flow at time i.

Steps in calculating

duration:

Step 1: Find present value of

each coupon or principal payment.

Step 2: Multiply this present

value by the year in which the cash flow is to be received.

Step 3: Repeat steps 1 and 2 for

each year in the life of the bond.

Step 4: Add the values obtained

in step 2 and divide by the price of the bond to get the value of duration.

Generally speaking, bond duration

possesses the following properties:

bonds with

higher coupon rates have shorter durations

bonds

with longer maturities have longer durations

bonds

with higher YTM lead to shorter durations

duration of a bond with coupons

is always less than its term to maturity because duration gives weight to the

interim payments. A zero-coupon bond’s duration is equal to its maturity.

Duration and

Immunisation

If the interest rate goes up, the

price of the bond falls but return on re-investment of interest income

increases. If the interest rate goes down, the price of the bond rises but

return on re-investment of interest income decreases. Thus the interest rate

change has two effects (price risk and reinvestment risk) in opposite

directions.

Can an investor ensure that these

two effects are equal so that he is immunised against interest rate risk? Yes,

it is possible, if the investor chooses a bond whose duration is equal to his

investment horizon. Forexample, if an investor’s investment horizon is 5 years, he

must choose a bond whose duration is equal to 5 years if he wants to insulate

himself against interest rate risk. If he does so, whenever there is a change

in interest rate, losses (or gains) in price is exactly offset by gains (or

losses) in re-investment.

Bond Portfolio

Management

The volatility of a bond is

determined by its coupon and maturity. The lower the coupon and the higher the

maturity, the more volatile are the bond prices. If market rates are expected

to decline, bond prices will rise. Therefore, you would want bonds with maximum

price volatility. Maximum price increase (capital gain) results from holding

long-term, low coupon bonds. (This is the same as saying hold bonds with long

durations).

If market rates are expected to

rise, bond prices will fall. Therefore, you would want bonds with minimum price

volatility. Therefore, invest in short term, high coupon bonds to minimise

price volatility and capital loss. (This is the same as saying ‘hold bonds with

short durations’).

Bond Theorems

- Price and interest rates move

inversely

- A decrease in interest rates

raises bond prices by more than a corresponding increase in rates lowers

the price

- Price volatility is inversely

related to coupon

- Price volatility is directly

related to maturity

- Price volatility increases at a

diminishing rate as maturity increases

Lets understand the theorems with illustrations:

Theorem-1 : Price and interest rates move

inversely

Lets assume 3 year 10% coupon paying bond for illustration

When YTM = 10%

|

Price = 100

|

When YTM = 11%

|

Price = 97.55

|

When YTM = 9%

|

Price = 102.53

|

Hence it can be concluded that as yield increase price of the

bond decline and vice-versa.

Theorem-2 : A decrease in interest rates

raises bond prices by more than a corresponding increase in rates lowers price

Lets assume 3 year 10% coupon paying bond for illustration

When YTM = 10%

|

Price = 100

|

|

When YTM = 11%

|

Price = 97.55

|

Change in price = -2.45%

|

When YTM = 9%

|

Price = 102.53

|

Change in price = +2.53%

|

This the most important theorem of bond which says that price

movement of bond with change is interest rate either side is not equal.

Price of the bond increases more than it declines when equal change in interest

rate is given. In above illustration you can clearly see that when yield

declines by 1% price increases by 2.53% while in case of increase in yield by

1%, price decline is 2.45%. As price curve of the bond is convex, you gain more

than you lose.

Theorem-3 : Price volatility is inversely

related to coupon

Lets assume 3 year 10% coupon paying bond and 3 year 11% coupon

paying bond for illustration.

3 year 10% coupon paying bond

When YTM = 10%

|

Price = 100

|

|

When YTM = 11%

|

Price = 97.55

|

Change in price = -2.45%

|

When YTM = 9%

|

Price = 102.53

|

Change in price = +2.53%

|

3 year 11% coupon paying bond

When YTM = 10%

|

Price = 102.48

|

|

When YTM = 11%

|

Price = 100

|

Change in price = -2.42%

|

When YTM = 9%

|

Price = 105.06

|

Change in price = +2.52%

|

Lets assume current YTM is 10% and then it increases to 11%

and declines to 9%. You can clearly see in the above tables that price

movement of the 11% coupon bond is lower than 10% coupon bond. It can be

concluded that higher coupon bonds are less volatile than smaller coupon bonds.

Bond Investment Strategies

Bond investors can choose from

many different investment strategies, depending on the role or roles that bonds

will play in their investment portfolios. Passive investment strategies include

buying and holding bonds until maturity and investing in bond funds or

portfolios that track bond indexes. Passive approaches may suit investors

seeking some of the traditional benefits of bonds, such as capital

preservation, income and diversification, but they do not attempt to capitalize

on the interest-rate, credit or market environment. Active investment

strategies, by contrast, try to outperform bond indexes, often by buying and

selling bonds to take advantage of price movements. They have the potential to

provide many or all of the benefits of bonds; however, to outperform indexes

successfully over the long term, active investing requires the ability to form

opinions on the economy, the direction of interest rates and/or the credit

environment; trade bonds efficiently to express those views; and manage risk.

Passive Strategies: Buy-and-Hold

Approaches Investors seeking capital preservation, income and/or

diversification may simply buy bonds and hold them until they mature. The

interest rate environment affects the prices buy-and-hold investors pay for

bonds when they first invest and again when they need to reinvest their money

at maturity. Strategies have evolved that can help buy-and-hold investors

manage this inherent interest-rate risk. One of the most popular is the bond

ladder. A laddered bond portfolio is invested equally in bonds maturing

periodically, usually every year or every other year. As the bonds mature,

money is reinvested to maintain the maturity ladder. Investors typically use

the laddered approach to match a steady liability stream and to reduce the risk

of having to reinvest a significant portion of their money in a low

interest-rate environment.

Another buy-and-hold approach is the barbell,

in which money is invested in a combination of short-term and long-term bonds;

as the short-term bonds mature, investors can reinvest to take advantage of

market opportunities while the long-term bonds provide attractive coupon rates.

Other

Passive Strategies

Investors seeking the traditional

benefits of bonds may also choose from passive investment strategies that

attempt to match the performance of bond indexes. For example, a core bond

portfolio in the U.S. might use a broad, investment-grade index, such as the

Barclays Capital Aggregate Bond Index, as a performance benchmark, or

guideline. Similar to equity indexes, bond indexes are transparent (the

securities in it are known) and performance is updated and published daily.

Many exchange-traded funds (ETFs) and certain bond mutual funds invest in the

same or similar securities held in bond indexes and thus closely track the

indexes’ performances. In these passive bond strategies, portfolio managers

change the composition of their portfolios if and when the corresponding

indexes change but do not generally make independent decisions on buying and

selling bonds.

Active

Strategies

Investors that aim to outperform

bond indexes use actively managed bond strategies. Active portfolio managers

can attempt to maximize income or capital (price) appreciation from bonds, or

both. Many bond portfolios managed for institutional investors, many bond

mutual funds and an increasing number of ETFs are actively managed. One of the

most widely used active approaches is known as total return investing, which

uses a variety of strategies to maximize capital appreciation. Active bond

portfolio managers seeking price appreciation try to buy undervalued bonds,

hold them as they rise in price and then sell them before maturity to realize

the profits – ideally “buying low and selling high.” Active managers can employ

a number of different techniques in an effort to find bonds that could rise in

price.

Credit

analysis: Using

fundamental, “bottom-up” credit analysis, active managers attempt to identify

individual bonds that may rise in price due to an improvement in the credit

standing of the issuer. Bond prices may increase, for example, when a company

brings in new and better management. n Macroeconomic analysis: Portfolio

managers use top-down analysis to find bonds that will rise in price due to

economic conditions, a favorable interest-rate environment or global growth

patterns. For example, as the emerging markets have become greater drivers of

global growth in recent years, many bonds from governments and corporate

issuers in these countries have risen in price.

Sector

rotation:

Based on their economic outlook, bond managers invest in certain sectors that

have historically increased in price during a particular phase in the economic cycle

and avoid those that have underperformed at that point. As the economic cycle

turns, they sell bonds in one sector and buy in another.

Market

analysis:

Portfolio managers can buy and sell bonds to take advantage of changes in

supply and demand that cause price movements.

Duration

management:

To express a view on and help manage the risk in interest-rate changes,

portfolio managers can adjust the duration of their bond portfolios. Managers

anticipating a rise in interest rates can attempt to protect bond portfolios

from a negative price impact by shortening duration, possibly by selling some

longer-term bonds and buying short-term bonds. Conversely, to maximize the

positive impact of an expected drop in interest rates, active managers can

lengthen duration on bond portfolios.

Yield

curve positioning: Active

bond managers can adjust the maturity structure of a bond portfolio based on

expected changes in the relationship between bonds with different maturities, a

relationship illustrated by the “yield curve.” While yields normally rise with

maturity, this relationship can change, creating opportunities for active bond

managers to position a portfolio in the area of the yield curve that is likely

to perform the best in a given economic environment.

Roll

down: When

short-term interest rates are lower then longer-term rates (known as a “normal”

interest rate environment), a bond is valued at successively lower yields and

higher prices as it approaches maturity or “rolls down the yield curve.” A bond

manager can hold a bond for a period of time as it appreciates in price and

sell it before maturity to realize the gain. This strategy can continually add

to total return in a normal interest rate environment.

Derivatives: Bond managers can use

futures, options and derivatives to express a wide range of views, from the

creditworthiness of a particular issuer to the direction of interest rates. An

active bond manager may also take steps to maximize income without increasing

risk significantly, perhaps by investing in some longer-term or slightly lower

rated bonds, which carry higher coupons.

Active

vs. Passive Strategies

Investors have long debated the merits of

active management, such as total return investing, versus passive management

and ladder/ barbell strategies. A major contention in this debate is whether

the bond market is too efficient to allow active managers to consistently

outperform the market itself. An active bond manager, such as PIMCO, would

counter this argument by noting that both size and flexibility help enable

active managers to optimize short- and long-term trends in efforts to

outperform the market. Active managers can also manage the interest-rate,

credit and other potential risks in bond portfolios as market conditions change

in an effort to protect investment returns. A word about risk: Past performance

is not a guarantee or a reliable indicator of future results. Investing in the

bond market is subject to certain risks including market, interest-rate,

issuer, credit, and inflation risk; investments may be worth more or less than

the original cost when redeemed. Investing in foreign denominated and/or

domiciled securities may involve heightened risk due to currency fluctuations,

and economic and political risks, which may be enhanced in emerging markets.

Mortgage and asset-backed securities may be sensitive to changes in interest

rates, subject to early repayment risk, and their value may fluctuate in

response to the market’s perception of issuer creditworthiness; while generally

supported by some form of government or private guarantee there is no assurance

that private guarantors will meet their obligations. High-yield, lower-rated,

securities involve greater risk than higher-rated securities; portfolios that

invest in them may be subject to greater levels of credit and liquidity risk

than portfolios that do not. Duration is the measure of a bond’s price

sensitivity to interest rates and is expressed in years.

Comments

Post a Comment